Understanding Your Options: Borrowing Strategically Against Your Assets

Borrowing against your assets can be a strategic way to access liquidity without disrupting your investment portfolio. Here are three primary methods to leverage your assets: Home Equity Lines of Credit (HELOCs), Margin Loans, and Securities-Based Lines of Credit (SBLOCs). Here's an overview of each option:

1. Home Equity Line of Credit (HELOC)

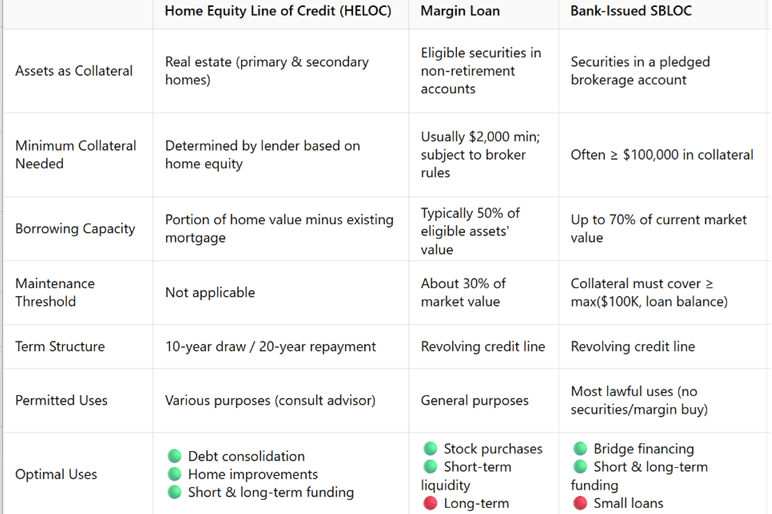

What It Is: A HELOC allows you to borrow against the equity in your home, providing a revolving line of credit that you can draw from as needed.

Key Features:

Collateral: Your primary or secondary residence.

Borrowing Limit: Determined by the appraised value of your home minus any existing mortgage balance.

Interest Rates: Typically variable and often lower than those of credit cards or personal loans.

Usage: Funds can be used for various purposes, such as home renovations, debt consolidation, or large purchases.

Tax Considerations: Interest may be tax-deductible if used to "buy, build, or substantially improve" the property securing the loan, subject to IRS limitations.

Considerations: Applying for a HELOC involves a home appraisal and underwriting review, which can take several weeks. It's advisable to apply well before the funds are needed. Additionally, since your home is used as collateral, failure to repay could result in foreclosure.

2. Margin Loan

What It Is: A margin loan allows you to borrow against the value of eligible securities in your brokerage account, such as stocks, bonds, ETFs, and mutual funds.

Key Features:

Collateral: Eligible securities in a non-retirement brokerage account.

Borrowing Limit: Typically up to 50% of the value of marginable securities.

Interest Rates: Variable rates that may be lower than unsecured lending options.

Usage: Funds can be used for various purposes, including purchasing additional investments or covering short-term liquidity needs.

Tax Considerations: Interest paid may be tax-deductible if the borrowed funds are used to purchase taxable investments and you itemize deductions.

Considerations: If the value of your securities falls below a certain threshold (maintenance requirement), you may face a margin call, requiring you to deposit more funds or sell assets to cover the shortfall. This can lead to potential losses and tax implications.

3. Securities-Based Line of Credit (SBLOC)

What It Is: An SBLOC, such as Schwab Bank's Pledged Asset Line®, allows you to borrow against the value of your investment portfolio without liquidating assets.

Key Features:

Collateral: Eligible non-retirement securities held in a separate pledged account.

Borrowing Limit: Based on the loan value of pledged securities, typically up to 70% of their current market value.

Interest Rates: Variable rates, often competitive with other lending options.

Usage: Funds can be used for a variety of purposes, such as real estate purchases, tax payments, or business expenses.

Tax Considerations: Unlike margin loans, interest on SBLOCs is generally not tax-deductible.

Considerations: SBLOCs are "non-purpose" loans, meaning they cannot be used to purchase or carry securities or to repay margin loans. Additionally, if the value of your pledged securities declines, you may be required to provide additional collateral or repay the loan, and failure to do so could result in the liquidation of your assets.

Final Thoughts

Each borrowing option has its own advantages and risks. HELOCs are suitable for homeowners seeking flexible funding for various needs. Margin loans can be beneficial for investors looking to leverage their portfolios for additional investments. SBLOCs offer a way to access liquidity without selling investments, preserving your long-term financial strategies.

Before proceeding with any of these options, it's crucial to assess your financial situation, risk tolerance, and investment goals. Consulting with a financial advisor can help you determine the most appropriate strategy for your needs.

The information provided herein is intended solely for general informational purposes and should not be interpreted as personalized investment advice or an individualized recommendation. Investment strategies discussed may not be appropriate for every investor. Each individual should carefully evaluate any strategy in light of their unique financial situation before making investment decisions.

All opinions expressed are subject to change without notice in reaction to shifting market conditions. While data presented may come from third-party sources believed to be reliable, Mietzner Wealth Management cannot guarantee its accuracy, completeness, or reliability.

Any examples provided are purely illustrative and do not represent expected outcomes or guaranteed results.

If you are considering a margin loan, it's essential to determine whether using margin aligns with your overall investment strategy and risk tolerance. Margin investing carries inherent risk and requires a thorough understanding of the associated rules and requirements.

Trading on margin increases market exposure and can amplify both gains and losses. Losses can exceed the value of the collateral in your margin account.

There is no entitlement to an extension of time in the event of a margin call.

This content is general in nature and is not intended to provide specific legal, tax, or investment advice. Tax regulations may change, potentially with retroactive effect. For advice tailored to your individual circumstances, consult with qualified professionals such as a CPA, financial planner, or investment advisor before acting on any of the information provided.

Nothing in this material should be interpreted as a commitment to lend. All loans are subject to credit approval, property approval, and applicable terms and conditions.

Please consult your tax advisor to determine the deductibility of interest payments on a home equity line of credit based on your personal tax situation.

All investments involve risk, including the potential loss of principal.

May 16, 2025

Get in touch

Address

800 W El Camino Real, Ste 180

Mountain View, CA 94040

Contacts

408-786-5566

contact@mietznerwm.com

© 2025. All rights reserved.

Investment Advisory Services offered through Mietzner Wealth Management, LLC, a California Registered Investment Advisor.