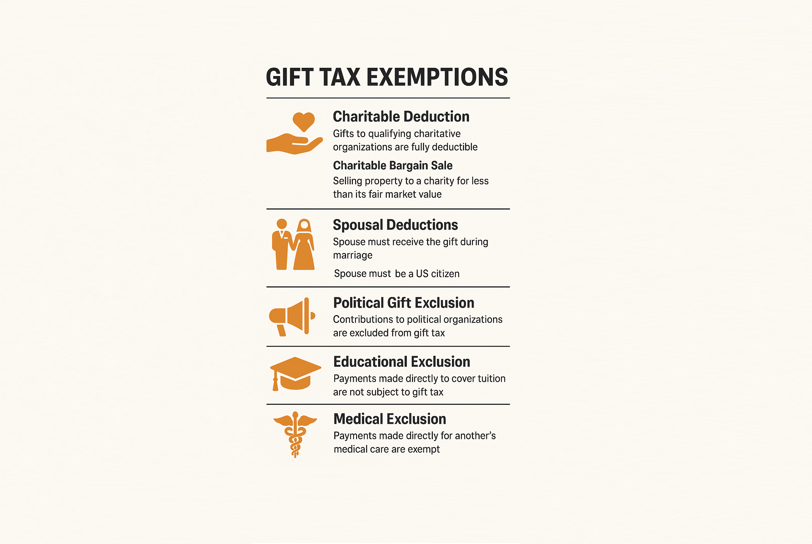

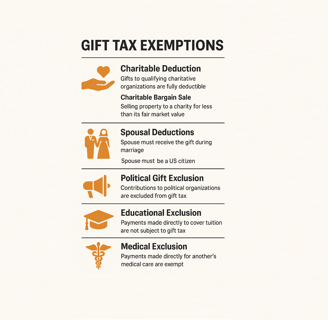

Understanding Gift Tax Exemptions

The U.S. tax code imposes a gift tax on the transfer of property by one individual to another without receiving full value in return. However, several important exemptions allow taxpayers to reduce or avoid this tax. This article covers key gift tax exemptions including charitable deductions, spousal deductions, political contributions, and exclusions for education and medical expenses. This content is general in nature and is not intended to provide specific legal, tax, or investment advice.

Jared Mietzner, CFP®

6/4/20253 min read

1. Charitable Deduction

Under IRC §2522, gifts made to qualifying charitable organizations are fully exempt from gift tax. To qualify, the recipient must be a 501(c)(3) organization or another recognized tax-exempt entity.

Charitable Bargain Sale

A charitable bargain sale occurs when property is sold to a charity for less than its fair market value. The difference between the sale price and the fair market value is considered a charitable gift and qualifies for the gift tax charitable deduction.

Key Considerations:

The donor must properly document the transaction.

The charity must be eligible under IRS rules.

Fair market value must be established via appraisal for non-cash property.

2. Spousal Deductions

The gift tax marital deduction under IRC §2523 allows an unlimited deduction for gifts between spouses, provided certain criteria are met.

Rules for Spousal Deduction Eligibility:

Gift must be made during the marriage – Gifts made before or after the legal marital period do not qualify.

No stipulation of termination – The gift cannot be a terminable interest that ends upon a future event (like divorce or death) unless it qualifies for QTIP treatment.

Spouse must be a U.S. citizen – Non-citizen spouses are subject to an annual exclusion limit ($190,000 in 2025, adjusted annually for inflation)..

If these conditions are not met, the gift may be subject to tax or limited exclusion treatment.

3. Political Organization Gift Exclusion

Contributions to political organizations are excluded from gift tax under IRC §2501(a)(4). These must be made to a political organization as defined under IRC §527.

Conditions:

The organization must be tax-exempt under §527.

The gift must be used for political campaign activities.

Gifts must not provide the donor with a direct or indirect benefit.

This exclusion only applies to contributions to organizations—not to individual candidates directly

4. Educational Exclusion

Under IRC §2503(e), tuition payments made directly to an educational institution for someone else are exempt from gift tax.

Key Rules:

Payments must be made directly to the school, not to the student.

Only tuition qualifies; room, board, books, and supplies are not included.

No dollar limit applies to this exclusion, as long as conditions are met

This strategy is often used in estate planning to transfer wealth efficiently while helping family member

5. Medical Exclusion

Also under IRC §2503(e), payments made directly to a medical provider for someone else's medical care are exempt from gift tax.

Eligible Medical Expenses Include:

Diagnosis, cure, mitigation, treatment, or prevention of disease.

Medical insurance premiums.

Long-term care expenses, if properly documented.

Requirements:

Payments must be made directly to the provider or insurance company.

Cosmetic procedures and indirect payments do not qualify.

6. Annual Gift Tax Exclusion

In addition to the specific exemptions discussed above, the IRS allows a general annual exclusion for gifts to any individual. This exclusion applies to the total value of gifts given to each recipient in a calendar year.

Key Facts:

For 2025, the annual exclusion is $19,000 per recipient.

This exclusion is per donor, per recipient. That means a married couple can jointly gift up to $38,000 to the same person in one year without triggering gift tax or needing to file a gift tax return.

The limit is adjusted for inflation periodically by the IRS.

Example:

You can give $19,000 to your son, $19,000 to your daughter, and $19,000 to a friend in the same year—none of those would count toward your lifetime gift tax exemption or require a gift tax filing.

This exclusion is the first line of defense in avoiding gift tax and is used in tandem with other strategies like charitable, educational, or medical exclusions to create a more tax-efficient transfer plan.

Final Thoughts

Understanding these exclusions is essential for effective estate and tax planning. The IRS rules are clear and favor well-documented, direct payments to qualified recipients. If done correctly, these strategies can significantly reduce taxable gifts and preserve family wealth.

The information provided herein is intended solely for general informational purposes and should not be interpreted as personalized investment advice or an individualized recommendation. Investment strategies discussed may not be appropriate for every investor. Each individual should carefully evaluate any strategy in light of their unique financial situation before making investment decisions.

All opinions expressed are subject to change without notice in reaction to shifting market conditions. While data presented may come from third-party sources believed to be reliable, Mietzner Wealth Management cannot guarantee its accuracy, completeness, or reliability.

Any examples provided are purely illustrative and do not represent expected outcomes or guaranteed results.

This content is general in nature and is not intended to provide specific legal, tax, or investment advice. Tax regulations may change, potentially with retroactive effect. For advice tailored to your individual circumstances, consult with qualified professionals such as a CPA, financial planner, or investment advisor before acting on any of the information provided.

Please consult your tax advisor to determine the deductibility of interest payments on a home equity line of credit based on your personal tax situation.

All investments involve risk, including the potential loss of principal.

Get in touch

Address

800 W El Camino Real, Ste 180

Mountain View, CA 94040

Contacts

408-786-5566

contact@mietznerwm.com

© 2025. All rights reserved.

Investment Advisory Services offered through Mietzner Wealth Management, LLC, a California Registered Investment Advisor.