Understanding Catch-Up Contributions: Maximizing Your Retirement Savings

Learn how 401(k) catch-up contributions work, who qualifies, and how recent changes under SECURE 2.0 affect savers aged 60 to 63. This guide breaks down 2025 contribution limits, helps you avoid common mistakes, and shows how to maximize every dollar toward your retirement goals.

Jared Mietzner, CFP®

7/9/20253 min read

How Much Can You Contribute to a 401(k) in 2025?

If you are serious about building long-term retirement security, you need to stay informed about contribution limits. Each year, the IRS adjusts the 401(k) thresholds to account for inflation. For 2025, the contribution caps have changed slightly, and there is a key addition for individuals in their early 60s that many people overlook.

Here is what you need to know.

Employee Contribution Limits for 2025

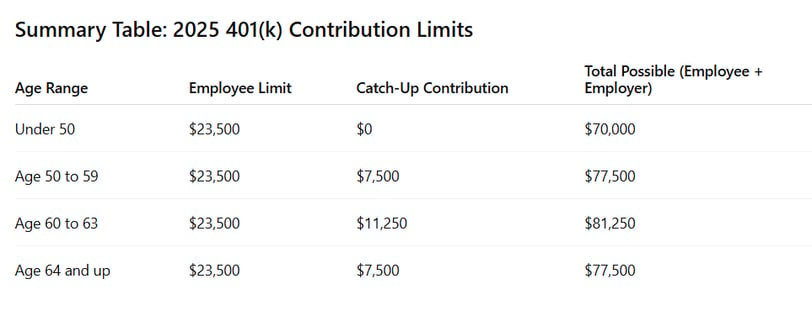

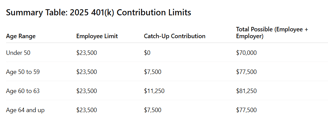

If you are under age 50, you may contribute up to $23,500 to your 401(k). This includes traditional pre-tax and Roth contributions.

If you are age 50 to 59, you can make a standard catch-up contribution of $7,500, for a total of $31,000.

If you are age 60 to 63, the SECURE 2.0 Act allows a special "super" catch-up contribution of $11,250, increasing your total allowable contribution to $34,750.

Once you turn 64, you revert to the standard $7,500 catch-up, just like those aged 50 to 59.

Total Contribution Limits (Including Employer Contributions)

The IRS also caps total contributions made by both the employee and the employer. These limits apply whether contributions are elective deferrals, employer matches, or profit-sharing.

If you are under age 50, the total limit is $70,000.

If you are 50 to 59 or 64 and older, the total cap is $77,500.

If you are 60 to 63, the total limit rises to $81,250, thanks to the higher catch-up amount.

Summary Table: 2025 401(k) Contribution Limits

Why This Matters

If you are not contributing up to these limits, you are leaving tax-deferred (or tax-free, in the case of Roth) growth on the table. These thresholds are not just best practices, they are legal maximums. Exceeding them can result in tax penalties and compliance issues for your plan.

It is especially important to be aware of the special rule for ages 60 through 63. Not all employers have updated their plans to support the new super catch-up provision. Make sure your 401(k) plan allows it before assuming you qualify.

Looking Back for Context

For comparison, the 2024 contribution limits were $23,000 for employee deferrals, with the same $7,500 catch-up for age 50 and up. The 2025 increase of $500 is modest, but historically consistent. The big change is the super catch-up for those in their early 60s, introduced under the SECURE 2.0 Act.

This is the first year that this provision is in effect. If you fall into the 60 to 63 age range, now is the time to take full advantage of it.

Final Thoughts

The government adjusts these figures every year, but the discipline of maxing out your contributions remains timeless. Know the limits, plan ahead, and check with your employer to confirm whether your plan allows for the full range of contributions, including catch-ups.

Saving for retirement is not about guessing. It is about precision, consistency, and using every tool the law allows.

Disclosures:

The information provided herein is intended solely for general informational purposes and should not be interpreted as personalized investment advice or an individualized recommendation. Investment strategies discussed may not be appropriate for every investor. Each individual should carefully evaluate any strategy in light of their unique financial situation before making investment decisions.

All opinions expressed are subject to change without notice in reaction to shifting market conditions. While data presented may come from third-party sources believed to be reliable, Mietzner Wealth Management cannot guarantee its accuracy, completeness, or reliability.

This content is general in nature and is not intended to provide specific legal, tax, or investment advice. Tax regulations may change, potentially with retroactive effect. For advice tailored to your individual circumstances, consult with qualified professionals such as a CPA, financial planner, or investment advisor before acting on any of the information provided.

Nothing in this material should be interpreted as a commitment to lend. All loans are subject to credit approval, property approval, and applicable terms and conditions.

Please consult your tax advisor to determine the deductibility of interest payments on a home equity line of credit based on your personal tax situation.

All investments involve risk, including the potential loss of principal.

Get in touch

Address

800 W El Camino Real, Ste 180

Mountain View, CA 94040

Contacts

408-786-5566

contact@mietznerwm.com

© 2025. All rights reserved.

Investment Advisory Services offered through Mietzner Wealth Management, LLC, a California Registered Investment Advisor.